📋 Table of Contents

Step 1: Appoint a Thai Accountant with CPD Status

Before you can begin Thailand company tax filing, you need a qualified accountant. Thai law requires that the person responsible for your company’s accounting holds a valid Continuing Professional Development (CPD) licence issued by the Department of Business Development (DBD).

Specifically, accountants must complete a minimum of 27 CPD hours per year, covering ethics, accounting standards, and professional skills. Moreover, a licensed accountant must sign all financial statements, making CPD verification an essential first step.

Why CPD Compliance Matters for Your Business

Financial statements signed by an unlicensed accountant are invalid. As a result, your annual company filing will be rejected by the DBD. Furthermore, the Revenue Department may disallow your tax deductions if the accounts are not properly maintained and certified.

When you partner with SMEBAAS accounting services, you can be confident that your accountant holds a current CPD licence and complies with all Thai accounting standards under the Financial Reporting Standards (TFRS).

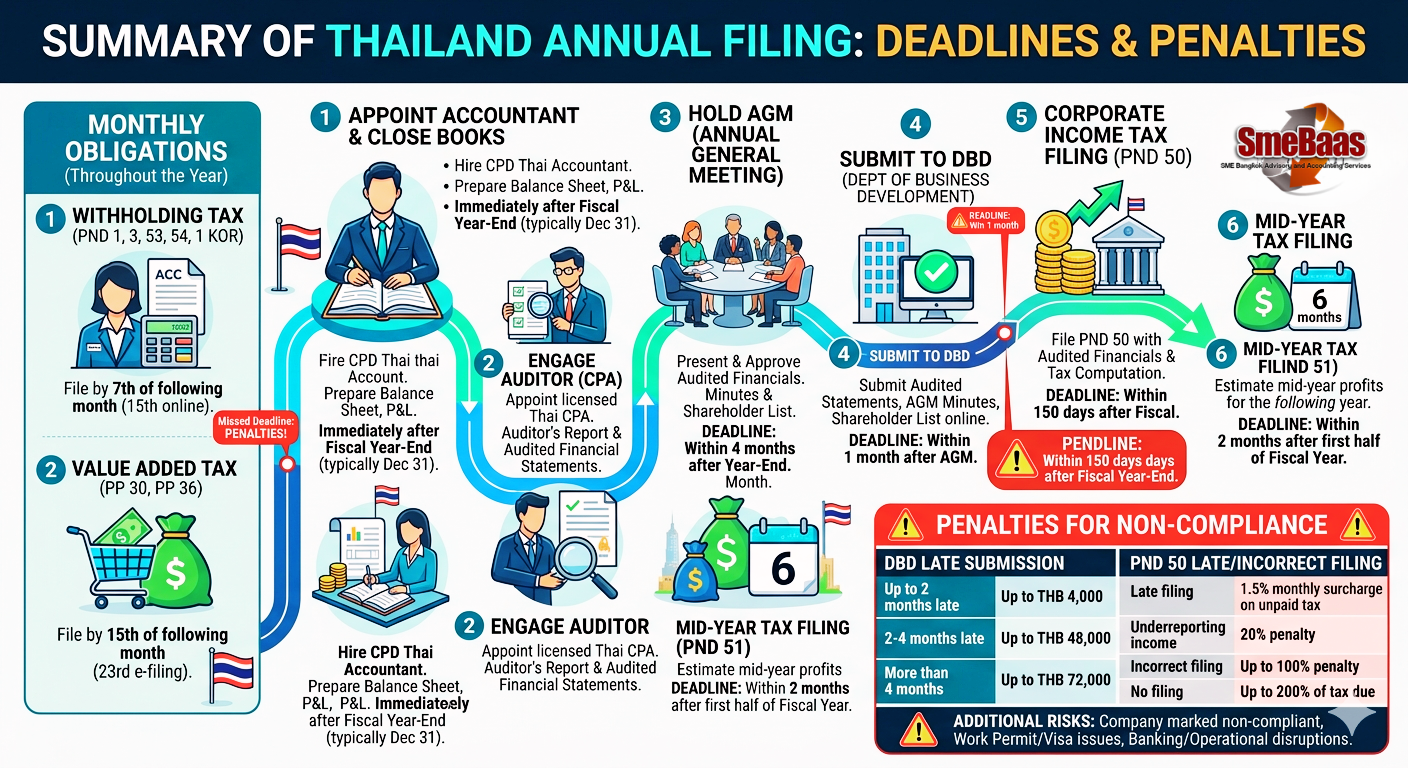

Step 2: Monthly Tax Obligations Throughout the Year

Beyond the annual and half-year deadlines, successful Thailand company tax filing depends on consistent monthly compliance. The Revenue Department expects companies to file and pay several taxes each month.

Monthly Withholding Tax — PND 1,3, 53, 54, and PND 1 KOR

PND 1 and PND 1 KOR covers withholding tax deducted from employee salaries. PND 3 covers withholding tax deducted from payments to individual service providers and contractors. Both forms must be filed by the 7th of the following month (or the 15th for online filing).

Furthermore, withholding tax deducted from payments to companies under PND 53, 54 follows the same monthly deadline. Therefore, tracking all payments to suppliers and service providers is a year-round responsibility.

Value Added Tax — PP 30, PP36

Companies registered for VAT must file PP 30 (VAT return) every month, reporting output VAT collected from customers and input VAT paid to suppliers. The net difference is either payable to or refundable from the Revenue Department. The filing deadline is the 15th of the following month (or the 23rd for e-filing).

Additionally, companies that provide services to foreign businesses may be subject to PP 36 reverse-charge VAT. Consequently, reviewing each payment category with your accountant ensures no VAT obligation is missed.

Step 3: Close the Books and Prepare Financial Statements

Most Thai companies follow a fiscal year from 1 January to 31 December. However, you can choose a different fiscal year if you register it with the Revenue Department from the start.

After the fiscal year closes, your accountant prepares the following financial documents: a Balance Sheet, a Profit and Loss Statement, a Statement of Changes in Equity, a Cash Flow Statement ( optional ), and supporting notes to the accounts.

Thai Financial Reporting Standards (TFRS)

All financial statements must comply with Thai Financial Reporting Standards. Therefore, your accountant must apply the correct TFRS framework — either full TFRS for listed companies, TFRS for NPAEs (Non-Publicly Accountable Entities) for private limited companies, or Thai Accounting Standards (TAS) for specific transactions.

As part of the Thailand company tax filing process, proper bookkeeping throughout the year significantly reduces the time and cost of year-end preparation. Consequently, businesses that maintain monthly management accounts enjoy a faster and more accurate annual close.

Step 4: Engage a Certified Auditor (CPA)

Thai law mandates that all registered limited companies have their financial statements audited annually by a Certified Public Accountant (CPA) licensed by the Federation of Accounting Professions (FAP). This requirement applies to virtually all juristic entities, regardless of size or revenue.

The auditor independently reviews your accounting records, confirms that the financial statements present a true and fair view, and issues an Auditor’s Report. Without this report, you cannot complete Thailand company tax filing with the DBD.

Requirement: The auditor must be independent of any other procedures in this process.

Choosing the Right Thai Auditor for Annual Tax Filing

Your auditor must be independent from your company — meaning they cannot also serve as your bookkeeper or management accountant. Additionally, the auditor’s FAP licence must be active and renewable. You can verify CPA licences on the FAP Thailand website.

SMEBAAS connects businesses with qualified, independent CPA auditors through its audit and assurance services. Accordingly, you receive both bookkeeping and auditing support under one coordinated service.

Step 5: Hold the Annual General Meeting (AGM)

Thai law requires all limited companies to hold an Annual General Meeting (AGM) within 4 months of the fiscal year-end. During the AGM, shareholders formally approve the audited financial statements, ratify dividends (if any), and re-appoint directors and auditors as needed.

The AGM must be properly convened with advance written notice to all shareholders — typically at least 7 days’ notice for a private limited company. Minutes of the meeting must be recorded and retained as part of the corporate records.

Step 6: Submit Audited Financial Statements to the DBD

After the auditor issues their report and the Annual General Meeting approves the accounts, your company must submit the audited financial statements to the Department of Business Development (DBD) under the Ministry of Commerce.

This submission is legally required under the Civil and Commercial Code of Thailand and constitutes a core part of annual company filing. Companies submit the statements online through the DBD’s e-Filing system or in person at the DBD office.

Documents Required for DBD Annual Filing

- Audited financial statements (balance sheet, P&L, cash flow, and notes) signed and approved by the company’s directors and shareholders

- Auditor’s report signed by a licensed CPA

- Directors’ report and resolutions from the AGM

- List of shareholders as of the AGM date

- BOJ 5 form — the official DBD annual submission form

Step 7: File Annual Corporate Income Tax (PND 50)

Filing the annual PND 50 form with the Revenue Department is the central step in Thailand company tax filing for most businesses. This form reports the company’s net profit and calculates the annual corporate income tax (CIT) liability. Visit page Corporate Income Tax page for more detail

PND 50 Filing Requirements and Attachments

- Completed PND 50 tax return form

- Audited financial statements attached as supporting documents

- Auditor’s report (required by the Revenue Department)

- Tax computation schedule reconciling accounting profit to taxable profit

Step 8: File Half-Year Corporate Income Tax (PND 51) for the following year

In addition to the annual PND 50, Thai law also requires companies to file a PND 51 form — a mid-year prepayment of corporate income tax based on estimated half-year profits. This interim payment helps the government collect tax revenue progressively throughout the year.

The estimated tax for PND 51 must equal at least 50% of the estimated full-year tax liability. If the actual annual tax (on PND 50) exceeds twice the PND 51 prepayment, the company faces a 20% surcharge on the shortfall. Therefore, accurate half-year profit estimates are essential.

Annual Compliance Timeline : Penalties for Late or Non-Compliance in Thailand Tax Filing

If you need assistance with any aspect of annual tax and company filing in Thailand, the SMEBAAS team is ready to help. Reach out through our contact page for a free consultation today.